Blackberry Q4 ´22 ER Review

Note: this is an update to my deep dive on Blackberry.

Summary: the business is progressing adequately. Lower guidance is a result of the licensing business no longer existing and of the way management is modelling cyber billings translating into revenue, none of which changes the long thesis.

Know thyself

We must be aware of the context Blackberry occupies on social media.

At first glance, the Q4 2022 ER looks boring and disappointing. Before we move on to look at the fundamentals, however, I want to go through a dynamic I am seeing unfold around Blackberry that I think is worth having in mind as a Blackberry investor.

As I was out and about yesterday night, I was trying to get a glimpse of the results. I could not find the link to the press release, so I resorted to Twitter. I have to say, my view got distorted quite severely by the massive amount of bearish / confusing $BB posts on Twitter.

After a 15 minutes of hesitantly sipping on my margarita, small talking and looking at my phone with one eye, I spotted that the large majority of these accounts were fake. Yet, I found their ability to swing my sentiment around the place to be remarkable.

Blackberry is a popular stock amongst retail investors (like myself), so the above mechanism at scale coupled with many retail investors not taking the time to read the ER transcript carefully, leads to the mirage we are seeing this morning.

The morale of this story is that we are often best off by taking the time to read and think carefully through the facts. Below, follows my take on the information Blackberry released yesterday. As always, I would much appreciate to hear any contrary thoughts.

Mindset check

The future is still RT-OS + UEM and Blackberry remains optimally positioned.

Just to spare you from reading my original Blackberry deep dive (although I still recommend going through it to get the most out of this post), the reason I am invested in the company is that I believe in the future, most things will be connected to the internet and Blackberry is uniquely positioned to make it happen, whilst underappreciated by the market.

In such a future, cyber attacks will have very serious implications in our physical world. Two key components to deal with this scenario are:

Real time operating systems (RT-OS)

Unified endpoint management (UEM)

RT-OS is about enabling machines / things to execute tasks with the highest degree of reliability possible. If we connect a car to the internet, for instance, we need to 100% make sure it runs as we expect it to, since it is a matter of life or death.

Once we connect a fleet of cars, for instance, we need to make sure no one car gets hacked, because the entire fleet may then be compromised and become hostile, putting many lives at risk. Within the fleet, each car is in effect an endpoint that we must secure, hence the importance of UEM.

The same applies to any device you may be able to think of. The combination of RT-OS and UEM creates a whole new world, in which machines tap into the growing collective intelligence of the internet and we let them do most of the work.

Blackberry shows great strength in both RT-OS and UEM, per the market signals that we can see today. QNX, its proprietary RT-OS, is used by 24/25 top electric vehicle OEMs and by Spacex. In turn, Blackberry´s UEM secures 18 of the G20 governments.

If you are long Blackberry, you likely know all of this. Still, I believe this is an important first step to look at yesterday´s results under the adequate light. What we are now looking for going forward is:

The above moat getting stronger

A growing revenue stemming from the moat

IoT

The moat continues to grow, despite considerable headwinds.

Bearing the above in mind, there is one fundamental thing I see the market not factoring in, which is sales cycles in both automotive and enterprise cybersecurity are long. Consider the remarks made by our Chen in yesterday´s call, when asked about the general embedded (RT-OS) market (versus auto embedded):

“General embedded, you see the production being a lot sooner on average, probably a couple of years out versus 6 or 7, or 5 or 6 years. So, -- and typically not as big in terms of dollar on the ASP, or it is a big organization like a hospital or medical devices, then the volume isn’t as big as the car industry. But it’s still very, very healthy.”

How often do you buy a car? Once every 5 years? Every 10 years? My point is, the connected car is not here yet and yet, quarter after quarter we kind of hope Chen will tell us the time has come, when we know it is at least 5 years away. Meanwhile, the RT-OS moat continues to grow, against the semi-conductor shortage and Ukraine war headwinds, preparing Blackberry for the future that lies ahead.

John Chen´s remarks (excuse me for copy pasting them, but they are highly relevant):

“I mentioned medical, that’s a really good field. We’re winning a lot. We have good momentum in there and because of the safety certification. There are other general embedded markets that are really not as economically exciting. That’s a fair way to say. So, we use -- we tend to stay away from those.”

“You may recall that over the last few years, we have seen a significant increase in the proportion of the QNX business from safety-critical foundation software, such as ADAS, advanced driver assist, digital cockpits and autonomous drive. This now constitutes the largest part of the total business, overtaking infotainment. This strategy to focus on functional safety plays to QNX strength and is validated by both, the market trends towards ECU consolidation as well as software-defined vehicle. We also see significant growth in safety-critical design opportunities in our pipeline.”

“We recorded 17, one seven, 17 new auto designs and 28 wins in the general embedded market. In Jan, we recorded wins in multiple verticals, including defense and aerospace, industry, industrial that is, as well as medical, our strongest GEM segment.”

Blackberry IVY, the 50:50 revenue split collaboration with $AMZN which will be the App Store of the world for connected cars is progressing adequately:

“IVY product development remains on track. And last month, we released the latest version of the product that is POC-ready.

The expectation is for successful POCs to lead to design wins, i.e., a commitment from customers to design IVY into vehicles. The CES demonstration also allowed us to showcase two of our many potential applications that IVY can enable, Car IQ in-vehicle payment and Electra’s AI-driven battery management application were both very well received by OEMs and are included in the IVY POCs.”

A second level thought here is that as Blackberry continues to cement its moat in the auto sector (RT-OS) for cars, this continues to draws OEMs towards Blackberry IVY. Blackberry charges one per unit of QNX sold to OEMs, but it can charge recurrently for data services provided to OEMs and drivers via IVY. Again, we are not there yet, but Blackberry continues to really boringly take the necessary steps in that direction.

Each quarter the market myopically looks at the beats / misses, totally missing the point. The game we are playing is naturally not suited to the human mind. We want results now and are by definition impatient, yet the future I describe is headed our way and the company continues to execute well, if you under the surface.

Cybersecurity

Billings are growing, yet revenue growth is still in the air. Key hires are recent and in general, Blackberry has just gotten started in the cyber game. Signs of product superiority continue to pop up.

On the cybersecurity front, things are less clear. Still, the key aspect is that sales cycles are long and there is much short term angst in today´s market.

Firstly, billings equate to future revenues, not revenues in the present. Blackberry is closing new billings in cybersecurity

“this was the third consecutive quarter of sequential billings growth. Billings not only grew double digits versus Q3, but they also increased year-over-year.”

yet the revenue is not showing up yet. Until we see the revenue coming in, however, the fundamental question of whether the management is executing well or not remains.

John Gianmatteo (head of cyber @ $BB, ex McAffee CRO) only joined the company a few quarters ago and since then, we have only heard of billings going up. I.e. as far as we can tell, the plan to make more money via cybsersecurity is proceeding adequately.

They are now hiring 250 more sales people, 150 for cybersecurity and 100 for IoT. We should see billings continue to go up. Per the natural length of the sales cycle, which is unknown to me at this point, we should see revenue go up accordingly. As it refers to other metrics like retention, I believe it is still too early to deduce anything from them.

Still, whilst I have great clarity in the RT-OS / IoT segment, I remain observant in the cyber segment. Still, we have some telling signs of progress. As it refers to the above moat (18 of G20 governments secured by Blackberry):

“It is also important to note that our leading security profile continues to resonate strongly with our large core customer base of the largest bank and government agencies. To reinforce this point, this quarter, we secured UEM renewal with the U.S. Air Force, the U.S. Department of Defense, the U.S. National Grid as well as a number of international governments including Poland Ministry of Foreign Affairs, Northern Ireland Department of Finance and Personnel, along with Swedish and Italian governments, just to name a few.” - John Chen

If Blackberry is good enough for the U.S. National Grid (read The Fifth Risk, by Michael Lewis, in which he takes readers on a tour of the US public organisms), then it is good enough for many companies. My original observation applies, Blackberry continues to demonstrate its cybersecurity prowess per the adoption of some of the world´s most important organizations, albeit public ones.

Another major trend is that John Chen continues to sing the “competitive win” song louder and louder. He was quite timid about it just a few quarters ago and now he is talking about them quite thoroughly. If Chen were like John Melo, whom I also think is a great CEO, I would not be that intrigued by his increasing pitch. Yet, Chen is a reserved man and when he speaks, he means something. List of competitive wins:

“The first is with a leading publicly traded medical supplies conglomerate based in the United States. The customer, like many others, was struggling to [serve] (ph) a 24/7 security operations centers and held a competitive tender process between BlackBerry, CrowdStrike and Arctic Wolf. They bought more than 10,000 license of our Guard-managed service due to BlackBerry performance and security credentials.”

“The second is with a leading manufacturer based in Asia that selected BlackBerry over CrowdStrike’s, Fortinet and Carbon Black. Following a detailed POC, they selected BlackBerry because of our product’s strong performance, uncovering multiple threats during the trial. Legacy secure [ph] based vendors still account for a significant portion of the overall market, especially with SMB customers. This was always an area of focus for Cylance.”

“An example of the recent wins there was with logistic company that held a bake-off to replace their current McAfee and Microsoft Defender solution. After a vigorous assessment that included McAfee, Symantec and CrowdStrike, they bought approximately 2,000 -- 3 years license for our Guard Advanced product because we detected a number of threats that other didn’t and as well as providing a higher level of customer services.”

About the cybersecurity market, Chen is seeing “raw demand” growing and sees plenty of opportunities for predictive AI/ML based cyber solutions to replace signature based companies like McAfee, Symantec and Microsoft. Blackberry is still a “new borne” in cyber.

“Cylance is particularly strong in the mid-market, small, medium business mid-market. And I think we’re seeing our activity picked up quite nicely, partly because of the Guard software that we released, probably by now, it’s about a year. And so -- we could see that trend up continuously every quarter. And so the number is starting to become meaningful.”

Chen will also be announcing a new channel sales partner in the coming 90 days, so I look forward to seeing that.

Patents and Outlook

The patents are well sold if one accounts for the associated costs of operating them and the outlook is fine, with the market again fixating on short term candy.

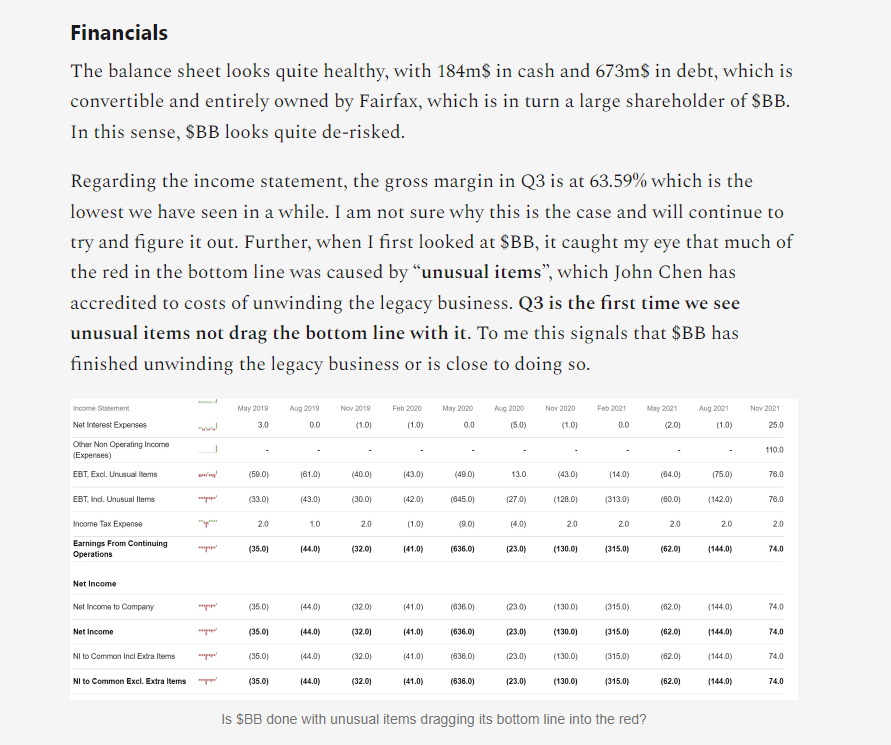

In the Q3 2022 ER review, I brought to your attention that “unusual items”, related to the unwinding of the legacy business, were dragging Blackberry´s bottom line (further) into the red than otherwise. I speculated that these expenses were coming to an end with the patent sale and so it has turned out. This is where a lot of the EPS surprise has come from (hello, sell side analysts).

When assessing the fair value of the patents Blackberry sold during this quarter for $600m, most were only looking at the revenue these patents were generating. The matter of the fact was that the costs associated to them were simply being accounted for as having nothing to do with Blackberry´s new business. Gone the patents (Blackberry phones), gone the expenses.

Note: $450m of the $600m was due at close yesterday.

Now Blackberry can use this cash to focus on what lies ahead: continuing to cement the RT-OS moat, bringing IVY to life and increasing cyber billings / revenue. When asked about this, John Chen said the same thing in his sometimes not very explicative words. I must admit he could do a better job at explaining the situation to investors and to the market. I totally understand why this exasperates investors who are not constantly scanning for and stitching details together:

“Okay. So, I would say, there’s still a lot of potential for this non core set of patents. But two things obviously you know. One is, time is ticking down in the validity of the portfolio. Although we have a very young -- we typically have, even with the non core, somewhere around 8 to 10 years type average lifetime with the patent still remaining. So -- but the -- if you notice that -- which you pointed out, the last couple of years -- or the last few years, we have some good success. But those are with very big names.

And so, now, we need to go -- the business needs to go cultivate pipeline for the smaller name, which typically takes a little longer time, a lot more back and forth. Big name does too, but big names have big numbers. So, in a way that the low-hanging fruit, we already approached. And so, I think the numbers we have done in market test the numbers, we think it’s very fair to both sides.”

As it refers to the outlook:

“licensing revenue is expected to be minimal”

“For the IoT business, we expect to see continued strong growth despite the ongoing headwind for the auto industry. We expect revenue for the year to be in the range of $200 million to $210 million, representing a 12% to 18% growth year-over-year.”

“For the cyber business, we expect to deliver billings growth between 8% to 12% this fiscal year, mainly as a result of increased traction from our security products. In fact, we expect to see higher billings in all four quarters when compared to the same quarter in the prior year.”

What the market did not like is the flat revenue growth projection, which seems to be due to the combination of the way management has modeled cyber billings translating into revenue with the disappearance of the licensing revenue:

“However, we model revenue for the year in total to be broadly flat year-over-year, factoring in the time for billings growth to convert to revenue.”

Either way, there seems to be nothing overly wrong with the business. True, we are still in the air regarding IVY and cyber revenue, but both the IoT and cyber segments seem to be progressing adequately, all things considered. In this occasion, it looks to me like the market does not like the uncertainty of the cyber sales life cycle, which is nonetheless just how life works.

Until next time!

PD. Looking forward to reading any constructive, well fundamented counter argument/s.

⚡ If you enjoyed the post, please feel free to share with friends, drop a like and leave me a comment.

You can also reach me at:

Twitter: @alc2022

LinkedIn: antoniolinaresc

Very interesting read and nice to see someone who understands where BlackBerry is headed. Smart Cars, smart cities, smart roads are a huge opportunity.

Having the world's best and most secure RTOS is something that will be used in more everyday items as the world continues to automate.

Cylance provides world class protection for all devices including computers and mobile.

In addition BlackBerry has many other valuable lines of business. Certicom, athoc just to name two.

Jarvis could be a huge product with the new rules and regulations for the software supply chain.

Unfortunately BlackBerry has a large number of amateur investors and a very small market cap and is easily manipulated.

Best thing as Buffet says is to buy and put it away - especially at these prices.

I agree with Dorman.

Antonio, can you shed some light on why Crowdstrike, a much younger company has been able to sell so much cyber security (they are booming) while BB with such a great product line is moving so slowly? Crowdstrike must have to deal with the same billings issues.

I've been long on BB for 10 years and it is frustrating to see us being left behind everyone else who seem to be thriving in today's environment.