Thoughts on $AMRS Q4 ER

Note: this is an update to my deep dive on $AMRS. I suggest you read it if you haven´t, to better understand the below.

Here is the format of today´s write up. Feel free to skip to whatever section you like.

1.Main Takeaway: I discuss why I think Amyris is going to see explosive growth and the challenge it is now facing.

2.Thoughts on Cost Optimizations and Manufacturing Capacity: I go through why I think management has what it takes, despite what the market thinks.

3.Financials: I go through the arbitrage that $AMRS today represents, together with an overview of its current financial health.

Disclaimer: the information contained in this write up is not intended to serve as financial advice. It is just my opinion and remember, there is no substitute to doing your own research. Also note that my minimum investment horizon is 5 years.

Finally, if you would like to stay even more up to date with my investing related thoughts, feel free to follow me on Twitter:

Main Takeaway

Brands are growing fast and are likely going to grow faster going forward. Now we just need cost optimization, which is going to require world class execution.

I believe we will see a much higher share price for $AMRS when the two following conditions are met:

Explosive, sustained brand revenue.

Costs are under control and sufficiently optimized to prove the company can be profitable.

I “disregard” other forms of revenue when hypothesizing about the market´s affection towards $AMRS. This is because the market likes predictable sources of revenue best and always finds plenty of excuses to disregard other forms of less predictable revenue. I do not like to bet on the latter either.

In fact, Amyris has now re-branded its ingredients business to “technology access”, as in giving other companies access to their technology. This makes sense and I think it will work eventually, because selling ingredients directly is not a dismissable business practice, in terms of cashflow generation.

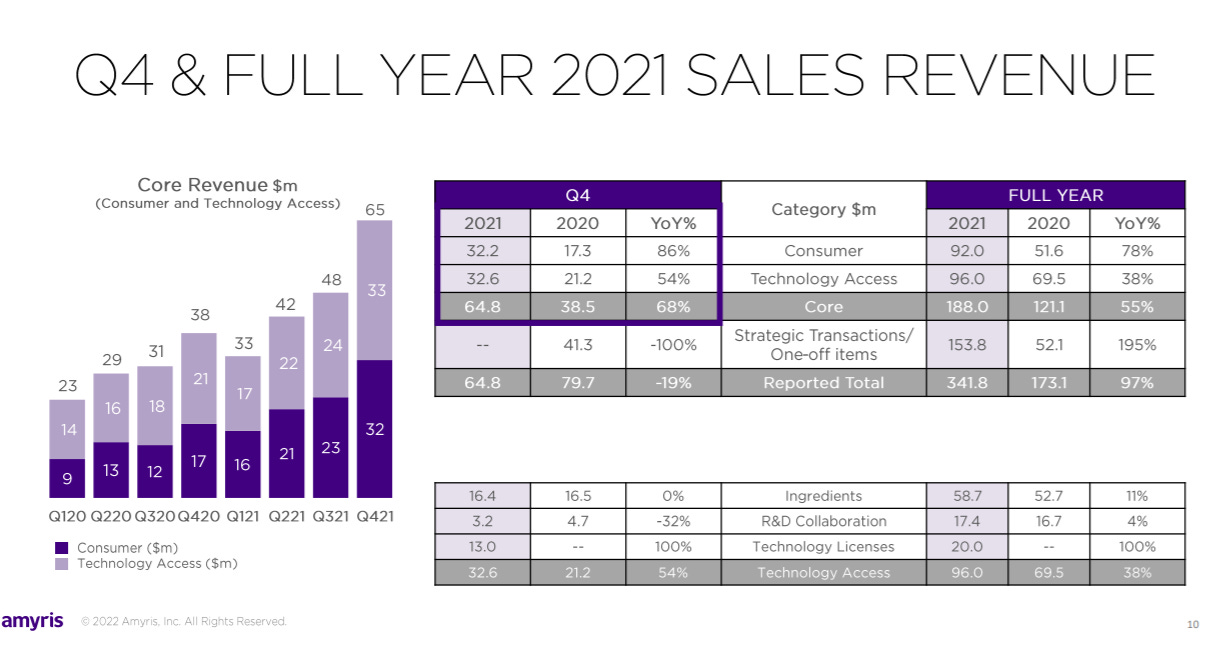

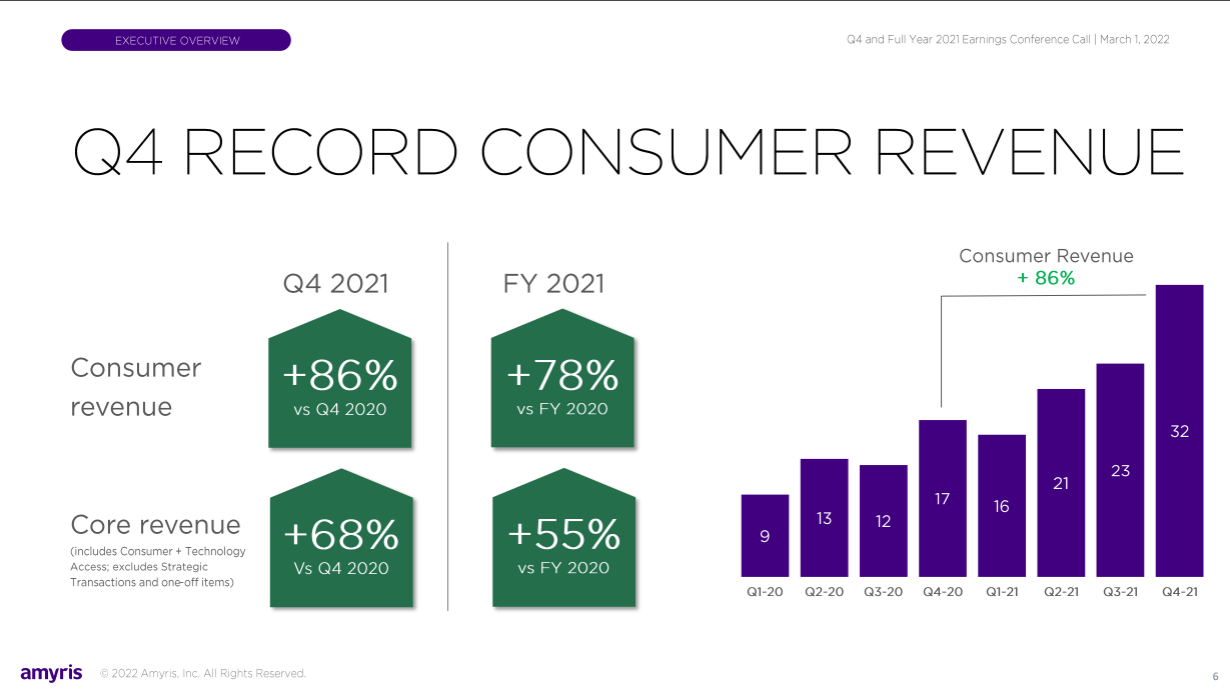

As you can see below, brand (consumer) revenue is growing very fast. At this stage, I believe this is empirical evidence of Amyris´ability to pick the right molecules to synthesize and then synthesize and commercialize them at scale sustainably and cost effectively (at least from the perspective of end consumers).

Management is forecasting 150% consumer revenue growth for 2022:

“First, accelerating consumer revenue growth, delivering much more than 150% growth versus last year, in 2022 with a very strong pipeline of new brands, new products, new markets to support this growth for well into the future.”

Here´s why I believe it:

As some of you know, I have been experimenting with Terasana these past few months, to treat the acne of a close relative. The results have been fantastic compared to alternative products in the market.

We are talking about a case of acne that has resisted pretty much all known forms of treatment. Terasana has cured the acne by:

De-inflammating the skin.

In doing so, enabling the skin to re-balance the biome and hence reduce the presence of “bad” bacteria, drastically reducing the lesions.

*Side note: I have also learned that biome imbalances in the skin are caused / augmented by imbalances in the gut´s biome, so we have achieved even better results by proceeding to address the latter, mostly by eliminating inflammatory foods such as gluten and introducing anti-inflammatory ones, such as curcumin.

Terasana is made of just CBG and squalane. Via traditional production methods, both would be prohibitively expensive for most end consumers and quite damaging to the environment. This is specially so in the case of squalane which involves killing sharks by default.

Terasana is a great example of how $AMRS is leveraging its capabilities to bring a vastly superior solution to market in terms of:

Effectiveness

Competitive pricing

Sustainability

How did Amyris manage to nail an acne solution? My reasoning is that, connecting the dots, this company seems to have some sort of a repeatable recipe to figure out how to disrupt the chemicals market ($3.4tr revenue in 2019) with superior products.

The top line is growing because this repeatable recipe is equating to ingredients / products with compelling value propositions and ultimately, into brands that are acquiring gravitas quite quickly. Management mentions this a couple of times throughout the call:

“We're actually seeing very strong growth beyond what we expected in vanillin. We're seeing very strong growth in Squalane, we're seeing very strong growth in Ambrox and Squalane.” - John Melo, CEO

“Perhaps, John, if I can have one comment to just give a little bit more color, because I think where you were headed is really to do with the underlying or the intrinsic growth around the ingredients, product portfolio.” -Han Kieftenbeld, CFO

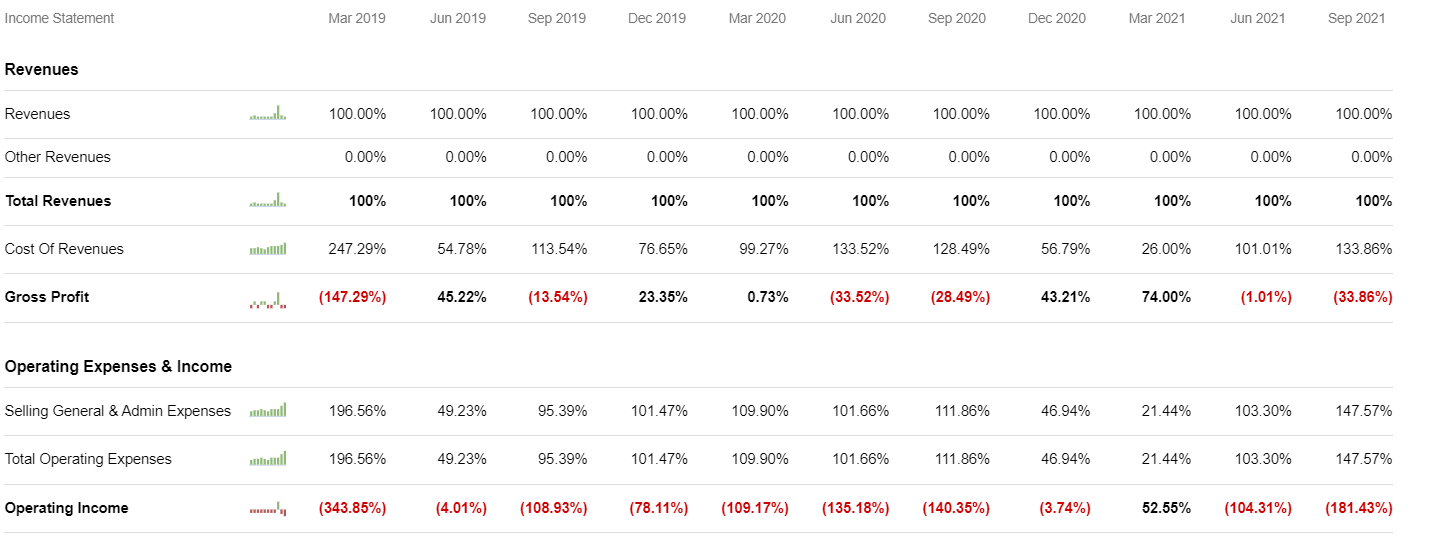

Having said that, the income statement is still a mess below the top line:

The plus side is that there is no cost optimization that can truly account for low growth. If you have fast growth, however, you have the luxury of tackling costs. The latter is where Amyris is at and I think is what is going to define whether the company makes it or breaks it.

Thoughts on Cost Optimizations and Manufacturing Capacity

I think the management has demonstrated the skills to pull this off. Amyris is way ahead the rest of the syn bio players and this means something.

Management has had their eyes on this task for a while, having begun the construction of their own manufacturing plants some time back. In the 9th of February, the company announced the new Reno consumer products plant commencing operations.

About the Barra Bonita ingredients plant in Brazil,

“Our new ingredients plant construction in Barra Bonita, Brazil has made great progress, and we are on track for the start of production early in the second quarter.” - John Melo

When these two plants are live, the company will effectively begin a supply chain verticalization journey, in which they will be gradually able to make the company´s operations leaner and maybe some day post a profit.

“As we noted, we have been investing substantially in the future of our core businesses. We expect the Barra Bonita ingredients plant and the Reno consumer production facility to be important drivers for gross margin improvement in the second half of this year.” - John Melo

The task ahead is enormously complex, but here is where I think we have to take a step back and just understand the bigger picture in synthetic biology, to shed some light on the management´s capacity, regardless of what the market may think about them.

There is no sufficient fermentation capacity in the world at the moment to fulfill the promises of other companies like Gingko Bioworks in the short to medium term and possibly the long term. The only syn bio company that has at-scale manufacturing capabilities today is Amyris. Amyris is now outputting at scale “three to five new molecules a year”, whilst other companies cannot do one.

For some reason, the call transcript is missing some bits from the actual call. During the call, I heard Melo (I believe) say that the new Barra Bonita plant will enable them to run various fermentation tanks in parallel, as if implying that previously they had to run tanks sequentially.

So whilst the world is yet to catch up with industrial fermentation 1.0, Amyris is moving on to 2.0. I recommend you watch the video I linked above to check for yourself that this is the case, together with the information from the call.

The point is, there is no way to guarantee that management will execute succesfully, but these guys have made it through one huge challenge after another to get to where they are. The market dislikes the company because the whole synthetic fuel promise was a flunk early on in the company´s public history and because management has so far tended to over promise and under deliver.

But the reality is, syn bio is making products that are gaining meaningful traction in the market place and Amyris is leading the industry, mostly due to the way it has been managed. Melo himself said in the call:

“I'd say we're probably 10 years ahead of DNA from an engineering and scale up and being able to really deliver real products to market”

As an end note to this section, many have asked me why I think the company has tremendous long term potential. This is because the mechanism (fermentation) that Amyris is using today to synthesize molecules is the same that nature has used to create the entire biological reality that surrounds us, including ourselves.

If the company manages to survive in the long term, we will see it synthesize organisms a decade or two from now. Think smartphones, cars and houses made through biology.

Financials

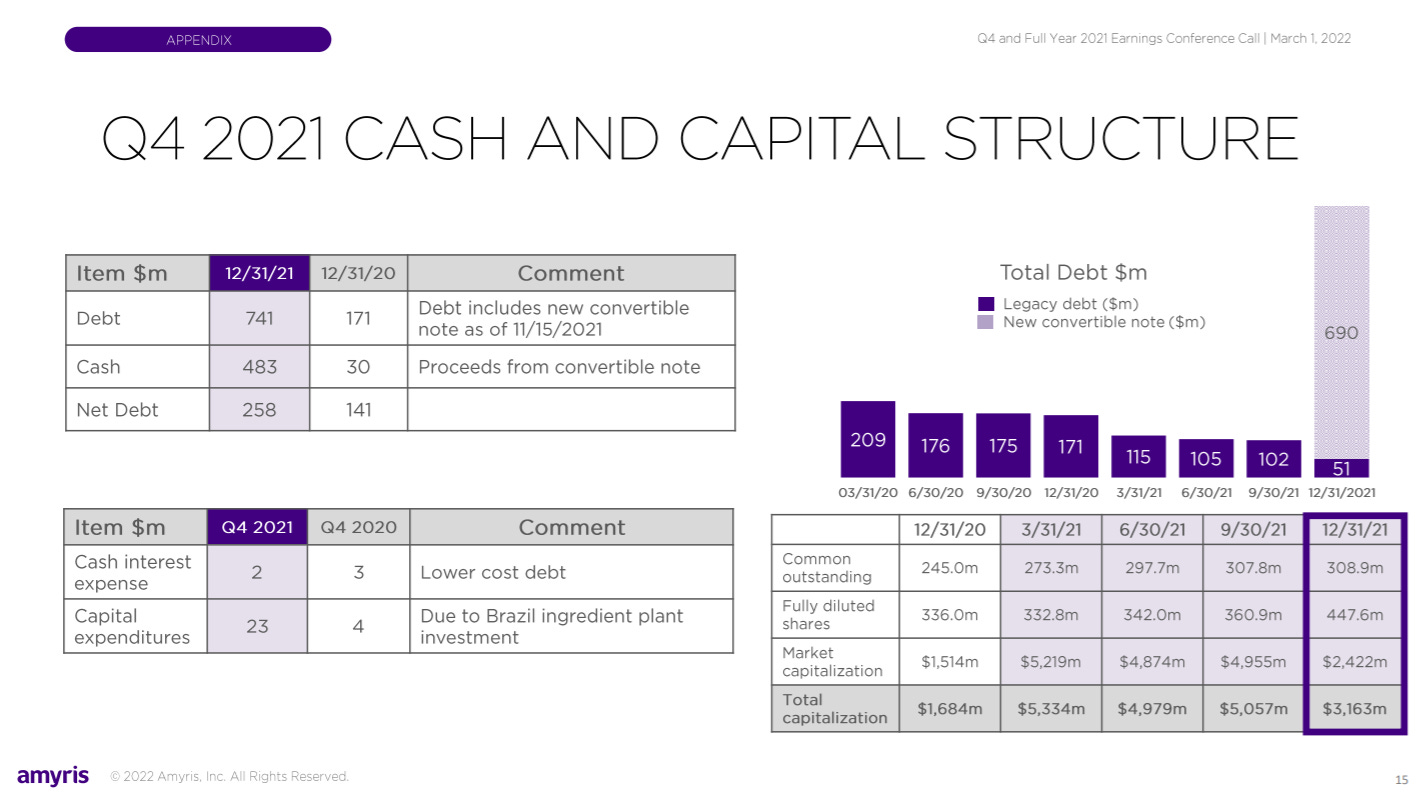

At today´s prices you are paying around $600m for the manufacturing capacity that the entire industry depends on. The company still depends on external financing, however.

$AMRS still trades today at a very reasonable price. The arbitrage is the same that I outlined in my deep dive.

Say its consumer brands could be valued at 10x revenue, which in the TTM cashed in $92m. Their brands could be valued collectively at $920m, given their performance in the past year. This is ignoring the 150% growth we may see in 2022.

The company´s market cap today is $1.5b, which means you would be paying just $600m for a manufacturing capacity / know how that $DNA ($6.4b mkt cap) is totally, even more so considering the “on-demand” / AWS for syn bio model they are pursuing. I can envision $DNA paying twice this amount to solve their current lack of capacity.

About financial health, the balance sheet is not made of steel but it is not terrible either. Per its operating cashflow, if sales do take off as the management says I think the company may not need to continue diluting shareholders. During the call, Melo said:

“We have no current plans for additional capital raises”

and about over-delivering and under-promising

I think the second thing is if you burn a few times, you learn quickly, so you can imagine we have quite a bit of cushion in our guidance.

I guess we will see if they have learnt that particular lesson.

On the other hand, it is worth noting that this is not a company in a stable situation and relies on external financing. The risk is high, but so is the potential return.

Until next time!

⚡ If you enjoyed the post, please feel free to share with friends, drop a like and leave me a comment.

You can also reach me at:

Twitter: @alc2022

LinkedIn: antoniolinaresc

Hola Antonio, disculpa que te haga una pregunta quizás fuera del tema... has comprado el aceite de Terasa desde Europa? es que una persona cercana tiene un problema similar, pero al buscar el producto solo lo encuentro a la venta en USA.

El substack fantastico, se aprecia mucho tu insight. Saludos.