Spotify Q2 2022 ER Digest

This is an update to my original Spotify deep dive, Q1 2022 ER digest. Below, you can find the format of this post and as always, feel free to skip to any section of your interest.

1.0 Thesis Recap and Digest Summary

2.0 The Network and Ad Business

3.0 Financials

4.0 Conclusion

1.0 Thesis Recap and Digest Summary

An asymmetric play. The company continues to advance well this quarter.

Most people see SPOT 0.00%↑ as a music streaming app, but I see it as an increasingly intelligent and global audio network, in which nodes emit and/or consumer audio files, except that it has been instantiated with a vertical that is as relevant as it is poor in terms of its unit economics: music. As the company continues to pile on further verticals, such as podcasts, audiobooks and news the general perception of what the company is will quickly morph and so will its financial profile. In 10 years time, Spotify will likely be a search engine akin to Google, but for audio.

Adding subsequent cash-rich verticals at a marginal cost in a network with nearly 0.5 billion MAUs (and growing) is no easy task, but the company is ideally suited to take on this challenge given its unique organizational culture and structure, which effectively make it an optimization machine. The successful deployment of additional verticals in any digital environment is always an optimization game, in which the organization in question must take thousands of correct resource allocation decisions. There is no way to know which are the right decisions ex-ante, but there is a way to find them via incessant cost-effective iteration.

Against all odds, Spotify has fended off competitors such as Apple and Amazon, now enjoying an exponential advantage, generally. Spotify´s user experience is far better and this is due to its ability to iterate cost-effectively at any given point in time. At its core, the nature of the task ahead is no different than what Spotify has been doing for the past decade and a half. For this reason, I hold a particularly contrarian view within what is already a contrarian thesis, that all Spotify has to do is carry on.

As always, the actual value of an investment idea comes down to price. At today´s valuation, Spotify is priced as if it were going to remain a financially non-viable music streaming service. If the deployment of further verticals is successful, the pay-off from here will be asymmetric, as a result of an earning power orders of magnitude higher than today. Conversely, if the deployment fails, the downside is capped due to the growing power Spotify has in the music industry. In this quarter, I see the company progressing adequately.

2.0 The Network and Ad Business

As the network continues to grow and engagement is fostered across verticals, the ad business will likely explode, tracking a non-linear increase in engagement.

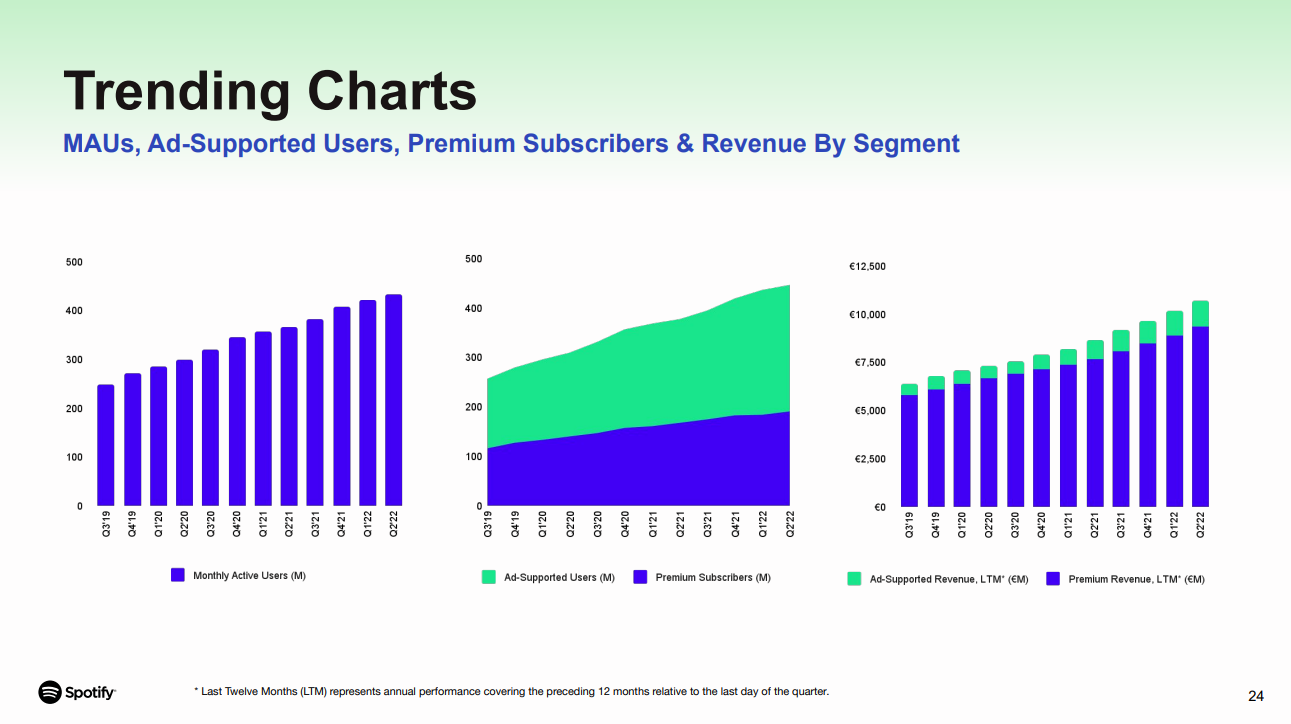

MAU growth seems to be largely immune to the macro environment, which speaks to the qualitative fact that Spotify actually plays a big role in people´s lives. The company is on track to hit the 1B MAUs that management is guiding to and growth is currently being driven by developing markets, where I believe the FC Barcelona deal (closed at the club´s financial lows) will do a great deal to nurture it. Premium subscribers came in 1M ahead of guidance, at 188M.

“… total monthly active users grew to 433 million in Q2. This result was 5 million ahead of our guidance and was the largest Q2 net additions in our history after adjusting for our exit from Russia and the March outage, which we discussed prior.” - CFO, Paul Vogel Q2 2022 ER

The engagement between nodes in the network today is low and mostly uni-directional. Consumers listen to creators and that is as far as it goes. However, the potential for further multi-dimensional engagement is pretty much endless, since consumers always want more from creators and vice versa. In the graph above you can see how ad-supported revenue continues to hit new records, but it remains largely limited by the current level of engagement. See Ek´s remarks on the topic below:

“So the number one part is still that a lot of our inventory just isn’t available to advertisers just yet. So we’re expanding the amount of inventory that’s available. That’s going to be by far the single biggest contributor to the growth of the ad business.”

“So, one of the best ways to actually get increased inventory is to increase engagement. So we are constantly improving testing products within the free offering and you will continue to see more innovation on the free side to drive more usage and more engagement, because we think that’s actually the best way to increase impressions.”

The other limiting factor to Spotify´s ad business is the actual ad-tech stack,

“… if you look at the acquisitions we have made, those have been geared towards bringing more measurement, more attribution, more personalization for advertisers. As ad-tech stack gets built out it will bring more people into SPAN.” - CFO, Paul Vogel

which the company is currently in the process of building out, mostly by integrating a string of acquisitions. In many ways, it seems like the company is advancing slowly, but the dynamics involved in dealing with a network of this size do not match other, more linear dynamics like the ones we experience in our day to day human lives. The company has been focused on user growth and now seems to be transitioning towards focusing on engagement and premium conversion. Ek calls this the “bandwagon effect”, by which user growth naturally translates into premium growth down the line - such is the wonders of a good product: Ek said in the call:

“But I think the general recipe is, the team has been very much focused for the past year in growing users.”

“…what we call the bandwagon effect at Spotify. [...] But what actually happens is we typically have gone between a sort of flip-flop of focus on each. […]If history is any indicator of the future, what will happen is, roughly a year from now, you’ll start seeing probably an acceleration in subscriber growth as evident from that.

New verticals per se are actually higher planes of engagement, apart “substantially differentiated” businesses in terms of gross margins, relative to the music vertical. You can listen to Bad Bunny´s music, but then you can also listen to a podcast featuring Bad Bunny, or an audio book about Bad Bunny and so forth. You are the same listener all along, but you are engaging with Bad Bunny along a staircase of audio verticals, each one opening the avenue for so many software features to drive further engagement. In effect, per every new vertical successfully deployed, engagement should tend to increase non-linearly.

There are plenty of mentions from management about the company now leaning further into overall experimentation and specially relating to new verticals. FY2023 should be exciting for Spotify shareholders:

“But the reality is you will probably see more of the full extent in the first half of ’23 of the audio book efforts. And it’s really kind of first half of ‘23 to second half of ‘23, you start seeing some of our work in some of the other categories.” - CEO, Daniel Ek

“But we are experimenting with them [categories]. We do plenty of experiments and bets internally and ‘23 will be a very big year for Spotify.”- CFO, Paul Vogel

3.0 Financials

The company is well equipped to carry on with its efforts to deploy further verticals.

Income Statement

The I/S has the same shape as it did in Q1. It will not meaningfully change until engagement is considerably increased. Beyond that, there are three things to note, although I believe neither will hurt the company in the long run:

OPEX is rising meaningfully, due to FX headwinds (“added nearly 1,000 basis

points of growth in expenses”) and increased salesforce and marketing expenses. Spotify is a European company with a large % of its OPEX denominated in USD, which makes me feel a bit uncomfortable with the way Europe is looking now

Historically, operating income tends to rise from Q2 to Q3. The guidance this time for Q3 is negative, for the reasons explained in point 1.

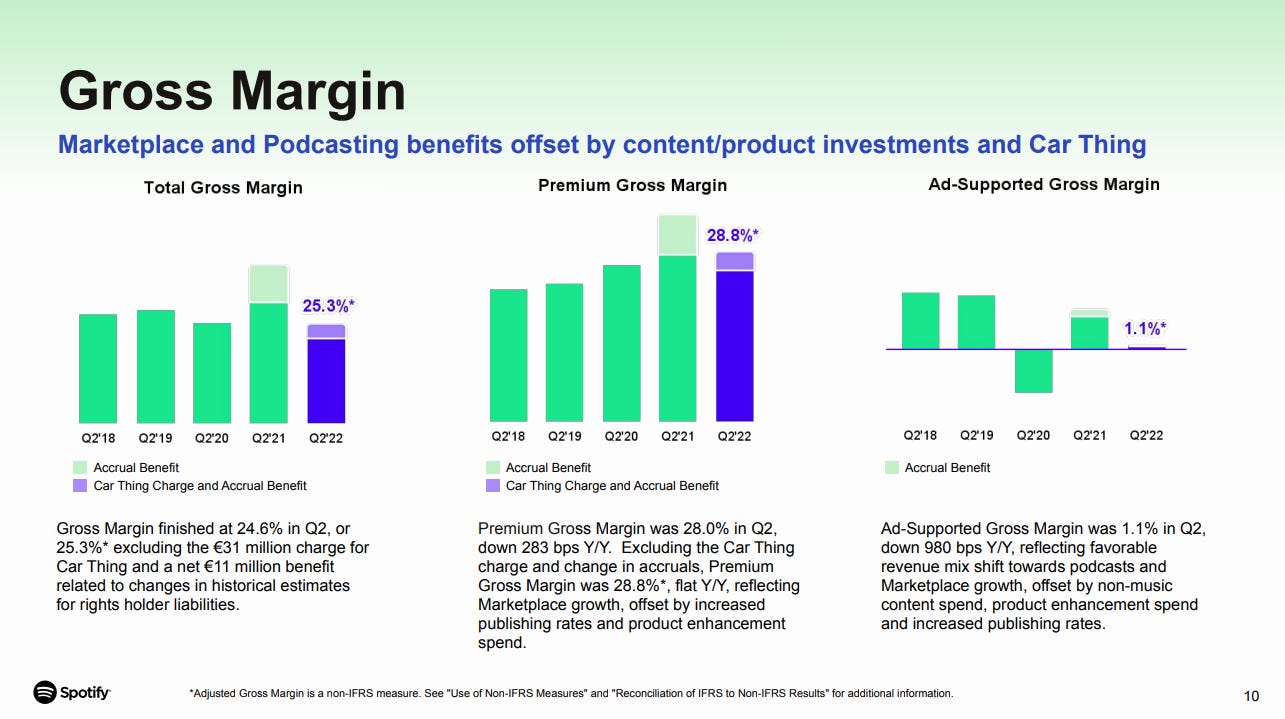

Car Thing was scrapped, with a one-time charge of $31m, impacting gross margin by 109bp.

Balance Sheet and Cashflow

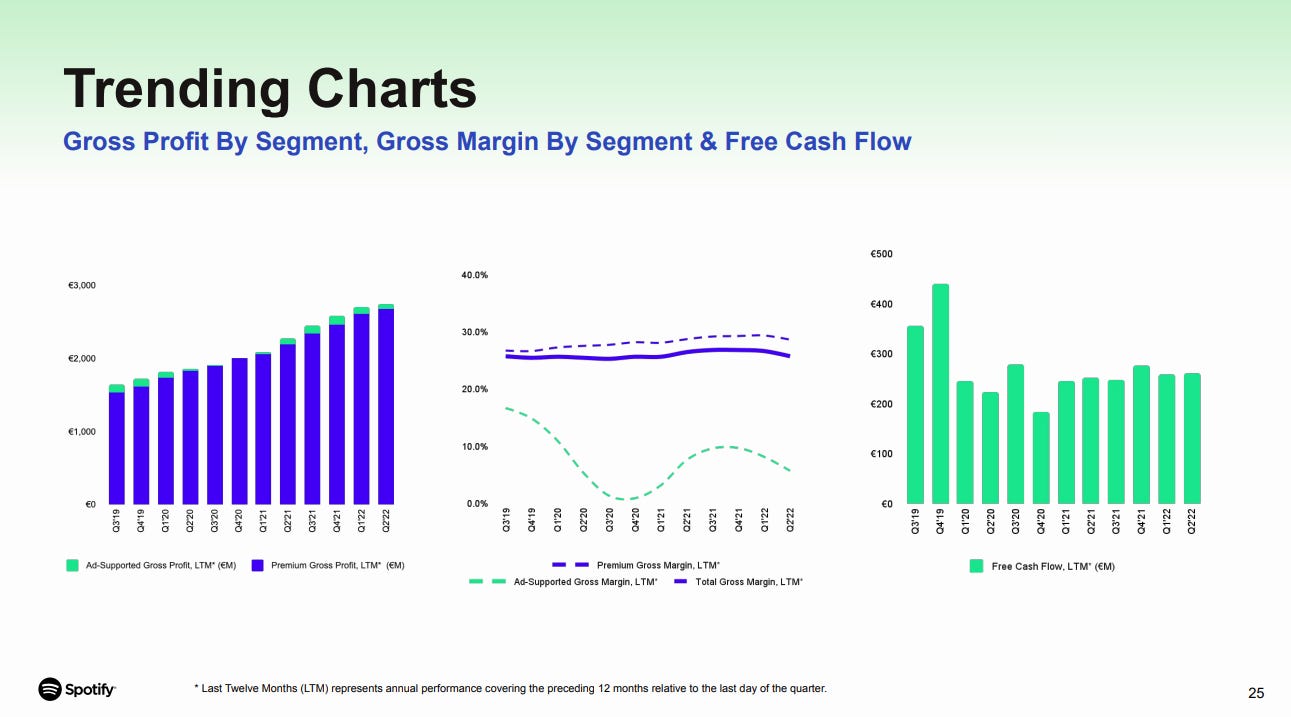

Spotify has plenty of dry powder:

It has $3b in cash and $1.1B in debt

and it produces cash continuously.

4.0 Conclusion

My thesis remains unchanged.

⚡ If you enjoyed the post, please feel free to share with friends, drop a like and leave me a comment.

You can also reach me at:

Twitter: @alc2022

LinkedIn: antoniolinaresc