GoPro Q1 ´23 ER Digest

Update

Edited by Brian Birnbaum and an update of my original GoPro deep dive.

1.0 The Turnaround Continues

Many of you will be surprised to see me covering GoPro, but perhaps you are not aware of the company´s turnaround that Bryan McGee has been overseeing with mastery. The company has pivoted towards a subscription business model that has turned it into a free cash-flow machine. With consumers pulling back across the board, the company´s financial performance has been shaved off at the margin recently, but, structurally, the company continues to evolve into a profitable, lean, and highly undervalued enterprise.

Its new strategy is very similar to that of Tesla´s: sell hardware at reasonable margins to then make most of the money via high margin software. GoPros are not for everyone, but they are particularly appealing for high end content creators. During the pandemic, when its customers where locked away, the company opted for the following strategy:

Eliminate entry level SKUs and focus on premium SKUs, increasing price of flagship camera by $100. This reduced the number of units shipped yearly.

Reduced retail presence by 30% globally.

Shifted to D2C, with sales via gopro.com going from 10% of total sales in 2019 to 38% in 2022.

Offered D2C customers a discount on cameras purchased, to funnel them into the subscription business for ~$50/year.

The combination of higher margins on the hardware side and the growing subscription business led to rapidly rising FCF levels, but there were still doubts about whether the subscription business was fake or not, since customers were offered a discount to opt it. My qualitative take, as you will find in my previous write ups on the company, is that the subscription deal is a no brainer for content creators. For the first time, this quarter we got some data on retention:

“In Q1, our first year renewal was between 60% to 65% and second year renewal was between 70% to 75%.” - Nick Woodman, CEO @ Q1 2023 ER.

So 60-65% of all the people that get funneled into the subscription service renew their subscription after 1 year and then 3/4 of them stay after another year. It seems like a reasonable funnel for a user base that gets baited into the service with a meaningful discount on a purchase. To improve its financial condition going forward, the company has to continue growing the number of subscribers. To do this, GoPro is now pursuing a post pandemic strategy, which consists in the following:

“Restoring pricing of our products to 2019 levels: MSRP reduction of $100 for our flagship HERO11 Black, HERO11 Mini, HERO10 Black and HERO9 Black cameras.

Re-introducing an entry-level price point SKU with HERO9 Black to drive meaningful volume and subscriber growth.

Restoring our world-class presence at retail. Our updated pricing and go-to-market strategy has been well received by retail partners

And eliminating camera discounts at the time of purchase at GoPro.com.”

This will apparently work because the retail attach rate is up big time, to approximately 50%, up 23% YoY and also because supply chains are starting to work normally again, with component costs coming down. The former means two things:

GoPro seems to be able to optimize processes now. I have been tracking them working on increasing the retail attach rate for a few years now and they are really making it happen.

It adds further evidence to support the idea that indeed the subscription business is real, since there are no discounts at retail for opting into the subscription. People seem to find it valuable on its own.

Therefore, as they pursue scale again on the hardware side, they should be able to populate the subscription service faster than otherwise. Further, the price reductions (as is the case with Tesla) lead one to suspect whether the products themselves are losing relevance in the market place. Despite the fear, which I too feel, I see no evidence of this happening just yet: the average selling prices of GoPro´s high end cameras have gone nowhere but up until this quarter. The same competitive scenario that I outline in the original deep dive seems to remain.

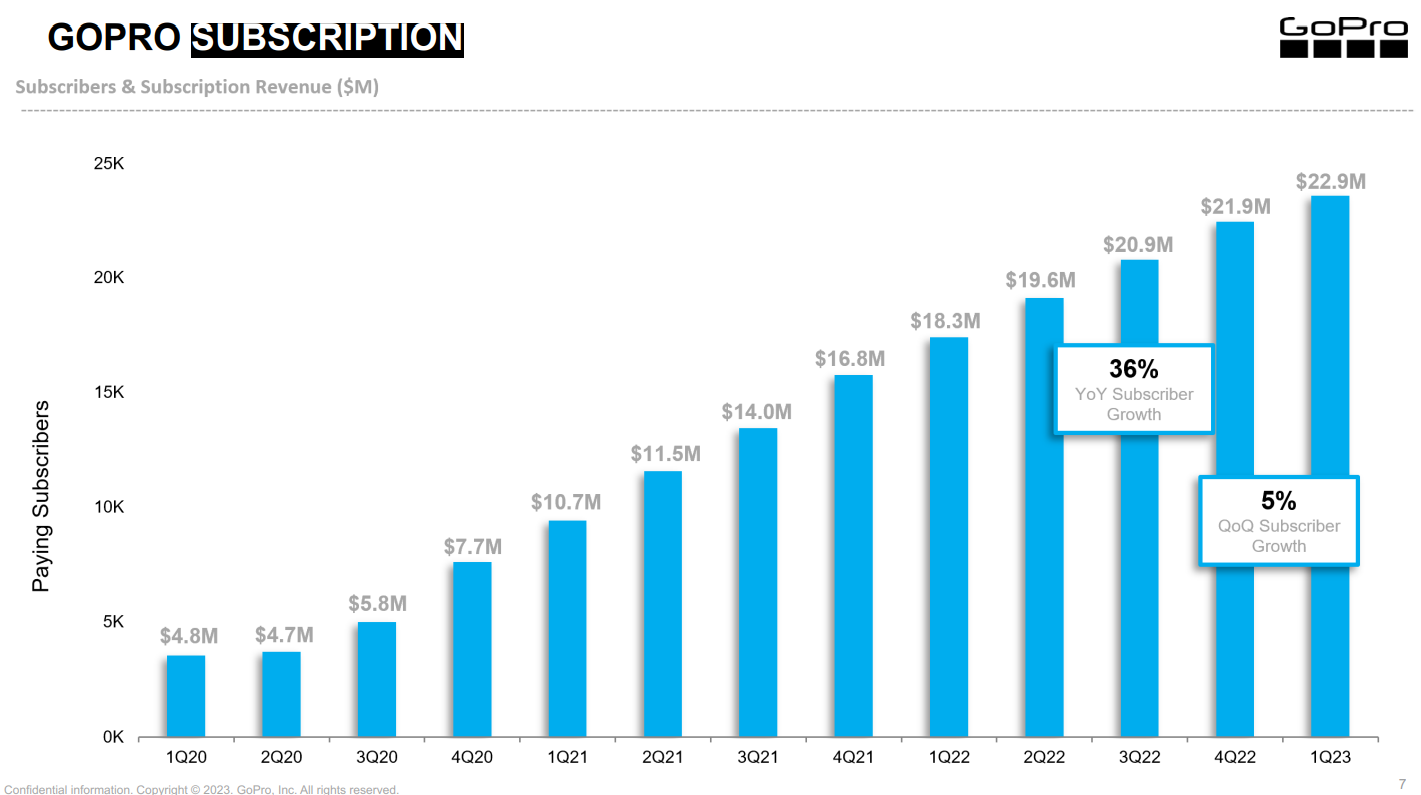

GoPro finished Q1 with 2.36M subscribers, up 5% QoQ and up 36% YoY. Management now expects to reach 2.45-2.6M subscribers in 2023, 2.7-2.8M subscribers in 2024, and 2.9-3.1M subscribers by the end of 2025. So far so good.

2.0 Margin Expansion

GoPro is now releasing:

A desktop editing experience that will be included in the current GoPro subscription at no additional charge.

A new premium subscription at Q4 2023, which management disclosed at the end of the last quarter would involve higher business volume and margins than the existing one.

I would have thought that the push towards scale on the hardware side would bring margins down, but according to management´s models margins will go up over the coming years. Indeed, funneling the scale into the subscription business is likely to fair well, so long as retention continues to improve. In that sense, I am glad to see the company continue to iterate on and improve the subscription offerings.

“And in '24, we would expect to continue with entry-level, but at cost points that actually would be margin positive versus not right now in '23. So, we have that going for us, and we'll have some newer products as well in '24 and '25, that help kind of round out kind of the overall demand and product profile for the company.

And that all leads to margins that -- to go up between 36% to 40%. And if currency goes back to 2021 levels, it's about 10%, you'd see margins in the kind of 39% to 43% range.” - Bryan McGee, COO @ Q1 2023 ER.

Before buying GoPro shares, I was aware of its turnaround strategy for some time, but I only bought in when I realized that McGee is a world class operator and that Woodman was happy to step down into a purely visionary role, which in my view he excels at. I have seen McGee turn the company into a free cashflow machine over the last few years, which has resulted in a phenomenally strong balance sheet. From 2021 to 2022 the company:

repaid $125 million in debt,

repurchased $40 million of our stock

and ended 2022 with cash of approximately $370 million,

with units shipped down more than 30%.

So long as the cameras remain relevant and McGee is in charge of operating the company, the thesis remains. My average is only just above current prices, so I am thus far happy with my position. Better days shall arrive economically speaking and GoPro will be ready to print cash again. The company is worth considerably more than the value for which it trades at today and as it continues to retire shares, a growing % of the value will accrue to shareholders.

⚡ If you enjoyed the post, please feel free to share with friends, drop a like and leave me a comment.

You can also reach me at:

Twitter: @alc2022

LinkedIn: antoniolinaresc